Businesses have always played an integral role in society. Whether it’s providing a service, distributing a product, or giving work to those in need, no one can deny that businesses contributed much to the country. But when you’re setting up a business, it’s easier said than done.

Most of the time, setting up a commercial organization is a sink-or-swim scenario. 20% of businesses will fail in their first year, while 50% will fail in their fifth year. What could be the reason why most of these businesses flopped after a few years? Most experts would say that they could not predict the current trends of the market, which makes it hard for them to adapt. Thus, it’s only essential that we emphasize our business’s planning phase before making any final decisions.

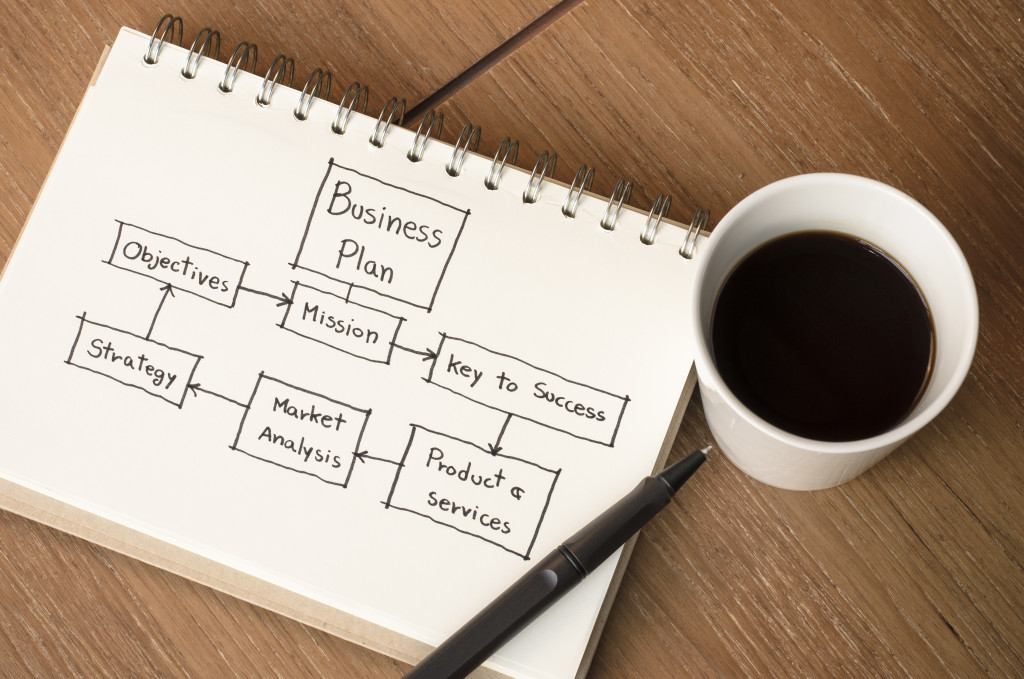

While most ideas might seem right in paper, there’s no guarantee that it will work well in execution. Thus, most business owners and investors will need to have a comprehensive plan and a sales pitch before anything else is done.

What Should It Include?

When you’re writing a business plan or making a pitch to different potential investors, it’s essential to ask yourself if it is feasible. Fortunately, there are separate sections when writing a business plan that will cover details, operations, and instruction for each step.

Still, your business plan shouldn’t be too wordy, complicated, or even complicated. Most of the time, getting straight to the point and being concise with your information is already enough.

Executive Overview

Firstly, the executive overview (or summary) will encompass the general idea of your business. That should come first in your business plan should outline everything that’s needed for your business. Naturally, this would encompass everything in just one to two pages.

When managing your new business, you must have consistent professionals that can give you much-needed information regarding your business ventures. Successful entrepreneurs would suggest hiring business advisors that are highly-qualified in providing insights to the business.

Opportunity for Inventory

Next, your business plan should have a section that will discuss the products and services you will advertise to clients. After choosing the product you’re confident with, you will need to know your target audience and the current trends.

Your business plan should also discuss the target market that you’re trying to get the attention of. One of the most effective means of identifying your target market is by knowing key market segments.

If you’re not familiar with TAM, SAM, and SOM definitions, here’s what you’ll need to know:

- TAM — This refers to the total available market or the demographic and market you are reaching out to.

- SAM — Served available market is a more narrowed down version for the total available market. Your SAM will explicitly target a portion of the total market.

- SOM — This is the market share, a narrowed down version of the SAM that realistically sets the number of individuals you can reach in the first few years.

Next, it’s best to discuss what’s trending as of the moment. There’s bound to be products that will usually always be in fashion while products and services will die down after a few months.

Competition and technological innovations can also come into play. However, this does not necessarily pertain to all types of products. For instance, experts predicted that smartwatches would make traditional watches obsolete, but this isn’t the case as conventional watches are still trending.

Execution

Right after you’ve already set your inventory, you’ll need to craft your marketing and sales plan, since this is essential in letting individuals be aware of your product.

But before you do make final decisions with your marketing plan, it’s crucial to define what your target demographic and market would be. If you’re not sure about who you are marketing to, there’s little chance that your product or service would succeed.

Operations

It’s also important to mention your day-to-day business operations. Logistics to your business will be the backbone of any known process. Of course, this will also depend on which type of industry your business. If the company is in programming and IT, you might have to invest in maintenance for servers, while companies in manufacturing will need to invest in industrial machinery.

In summary, setting up a business is a commitment that will take a reasonable amount of time, effort, and energy. Although at first, you might have to invest in making sure that your business will be successful, you must set realistic goals that you can achieve. That way, it’s easier to budget what you need for your capital and equipment.

While you’re in the process of planning, take your time. Although it might seem like you’re excited to have your business open, you’re essentially still in the planning stage, and you’re even not spending just yet.

Your business plan should be comprehensive and encompass everything that’s needed. Still, it should be too complicated that it can put off any potential investors and shareholders. Having a simple and easy-to-follow business proposal can ensure that everyone is on the same level of understanding.